How Zero-Spread Accounts Actually Work in Live Markets

Few features in retail forex and CFD trading generate more confusion than the zero-spread account. The name implies something appealing and apparently simple: no spread, no cost on entry, a cleaner trading environment. Yet traders who switch to zero-spread accounts without understanding the underlying mechanics sometimes find themselves paying more than they expected — or misreading the cost structure entirely.

The confusion is not a marketing accident. It reflects a genuine complexity in how zero-spread pricing is constructed, what replaces the spread as a cost mechanism, and how the model performs differently depending on what and how frequently you trade. Understanding that complexity requires looking at execution mechanics rather than account labels.

What 'Zero Spread' Actually Means

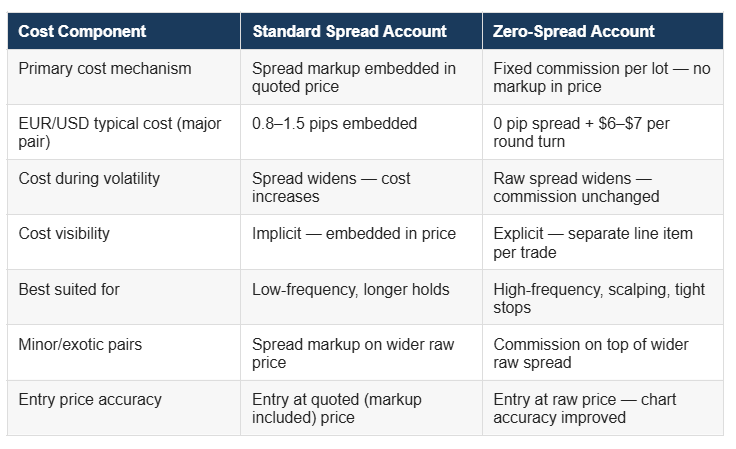

In standard retail forex pricing, the spread — the difference between the bid and ask price — is the primary cost of executing a trade. The broker quotes a slightly wider price than the raw interbank rate, and that markup is the cost embedded in the entry. No separate commission is charged; the spread is the fee.

A zero-spread account removes that embedded markup from the quoted price. The price you see is the raw or near-raw rate sourced directly from the broker's liquidity provider pool — the wholesale interbank price before any retail markup is applied. On major currency pairs during normal market conditions, this means spreads that genuinely reach or approach zero pips.

The critical clarification: zero spread does not mean zero cost. The cost mechanism has changed, not been eliminated. Instead of embedding the fee in the spread, the broker charges a fixed commission per lot traded — typically expressed in dollars per round turn (entry and exit combined) or per side.

This is the exchange at the heart of zero-spread pricing: spread markup out, explicit per-lot commission in.

How Commissions Replace Spread Mark-Ups

The commission structure on zero-spread accounts is straightforward in design. A trader opening and closing one standard lot (100,000 units) of EUR/USD might pay, for example, $7 per round turn — $3.50 on entry, $3.50 on exit. That $7 is the full cost of the trade on a zero-spread basis, regardless of whether the position is held for two seconds or two days.

Compare this with a standard spread account, where the same EUR/USD trade might carry a 1.2 pip spread. On a standard lot, one pip equals $10 — so a 1.2 pip spread represents $12 in embedded cost per round turn. On that comparison, the zero-spread commission account is meaningfully cheaper.

But the comparison depends entirely on what you are trading, when you are trading it, and how frequently. This is where the model's practical implications diverge based on trading style.

Zero-spread accounts do not eliminate the cost of trading — they restructure it. The fee moves from a variable component embedded in the price to a fixed, transparent, per-lot charge that applies regardless of market conditions.

When Zero Spread Is Beneficial

For high-frequency and scalping traders, the zero-spread model is typically the lower-cost option by a meaningful margin. A scalper executing 20 or 30 trades per day on EUR/USD is paying the spread cost on every single entry and exit. On a standard account, those accumulated spread costs compound significantly across a trading month. A fixed, lower commission per lot — charged regardless of how long the position is held — produces a materially lower total cost for this trading pattern.

For traders using tight stop-losses, zero spread improves the accuracy of entries. When the spread is embedded in the price, the position is immediately underwater by the spread amount at entry — the stop is effectively closer in pip terms than the chart appears to show. On a zero-spread account, entry is at the raw price, and the stop distance is what it looks like on the chart.

For news traders and event-driven strategies executed during normal conditions (not during the release itself), zero spread provides price clarity that standard markup accounts do not — the spread component is not silently amplifying entry cost.

When It May Cost More

For low-frequency traders — those placing a handful of trades per week on longer timeframes — the fixed commission per lot can actually exceed the equivalent spread cost on a standard account, particularly on pairs with already-tight standard spreads. A swing trader holding a position for several days incurs the commission cost once, but the spread on a standard account for a major pair during normal conditions may be similarly low.

For traders on minor or exotic pairs, zero-spread accounts may not offer the same advantage as on majors. Liquidity on these pairs is lower, the raw spread from liquidity providers is wider, and the commission layer adds on top — making total cost higher than on major pairs where raw spreads consistently approach zero.

For very small position sizes, the fixed commission per lot can represent a disproportionately high percentage of the position's potential profit — particularly for micro-lot traders where the math of commission vs spread needs careful calculation before assuming the zero-spread model is cheaper.

Market Volatility and Spread Widening

One of the most commonly misunderstood aspects of zero-spread accounts is their behaviour during volatility. The 'zero spread' label applies to normal market conditions when liquidity is deep and providers are quoting tight prices. During periods of significant market stress — major economic releases, geopolitical events, thin liquidity during off-hours — raw spreads from liquidity providers widen, and that widening is passed through to the trader.

This means a zero-spread account during the US Non-Farm Payrolls release or during an unexpected central bank intervention may carry a spread of several pips — the same or wider than a standard account during normal conditions. The zero in the account name is a normal-conditions description, not a guarantee across all market states.

Understanding this is important for managing expectations and for designing a trading strategy that accounts for real execution costs rather than best-case scenarios. Strategies built around the assumption of consistently zero spread — including all entries at the raw rate — will encounter real-world deviation during the conditions that often produce the largest price moves.

How TradeQuo Structures Its Zero-Spread Accounts

TradeQuo's zero-spread account structure is built on direct liquidity provider pricing passed through to the trader without additional markup — the raw interbank rate quoted to the account in real time. In place of spread markup, a fixed commission per standard lot applies to each round-turn trade.

The account operates under regulatory oversight through TradeQuo's licensed entities, with the pricing and execution model disclosed upfront in the platform's trading conditions — including the applicable commission rate, the instruments available on the zero-spread tier, and the expected spread range under normal and volatile market conditions.

For traders evaluating whether the zero-spread structure suits their approach, TradeQuo provides a cost comparison across account types within the platform's educational resources — allowing the calculation of total cost under different trading frequencies and position sizes before committing to a specific account structure.

Cost Transparency Comparison

Conclusion

Zero-spread accounts represent a genuine structural change in how trading costs are assembled — not the elimination of cost, but a shift from implicit, variable spread markup to explicit, fixed per-lot commission. That shift benefits certain trading styles significantly and makes little difference or even a marginal disadvantage for others.

The traders who benefit most are those who understand the mechanics: what replaces the spread, how volatility affects raw pricing, and how to calculate total cost across their actual trading pattern before assuming the zero-spread label translates directly to lower fees. That calculation — not the account name — is what determines whether the structure suits a particular approach.