The Psychology of Trading Costs: Why Small Spread Differences Matter Over Time

Traders spend significant time analysing entry signals, position sizing, and risk-reward ratios. The same rigour is rarely applied to the cost side of the equation the spread, commission, and markup that apply to every trade, regardless of outcome. This asymmetry in attention is a meaningful source of performance leakage, particularly for active traders operating across high volumes.

The reason small cost differences are underweighted is partly psychological and partly mathematical. Psychologically, a 0.3 pip difference in spread feels insignificant at the moment of execution. Mathematically, applied across hundreds or thousands of trades, it is not. Understanding how trading costs compound and how different cost structures interact with different trading styles is a more useful analytical exercise than most traders give it credit for.

How Small Costs Compound Over Time

The compounding effect of trading costs operates simply: every trade carries a cost that must be overcome before the position generates any net return. That cost is fixed relative to position size, applied at entry and exit, and accumulates linearly with trade frequency.

A trader executing 100 trades per month on EUR/USD with an average position size of one standard lot, on a spread-account with a 1.2 pip effective cost, is paying $1,200 per month in spread costs alone $14,400 per year before accounting for any commission or financing charges. Reduce that effective cost by 0.4 pips (to 0.8 pips) and the same trading volume costs $800 per month a $4,800 annual saving from a difference that feels negligible at the moment of any individual trade.

This is not a hypothetical edge case. It is the arithmetic of high-frequency retail trading, and it applies across any asset class where spread costs are the primary execution cost mechanism.

Spread vs Commission: Understanding the True Cost Structure

Retail trading accounts typically price execution in one of two ways. Standard spread accounts embed the broker's compensation in the quoted spread the difference between the bid and ask price includes a markup above the raw interbank rate. No commission is charged separately; the spread is the fee.

Raw or commission-based accounts quote at or near the interbank rate the spread approaches zero on major pairs during normal conditions and charge a fixed commission per lot traded, expressed as a dollar amount per round turn.

Neither structure is universally cheaper. The comparison depends on trading frequency and holding period. For active traders executing frequently, the fixed commission model tends to be more cost-efficient because the per-trade cost is lower than the accumulated spread markup across many trades. For lower-frequency traders holding positions for days or weeks, the per-lot commission may not represent a saving over the tighter spread on a standard account during normal conditions particularly if the standard spread is already competitive.

The relevant calculation is not 'which account type has a lower spread' but 'what is my total cost per month under each structure, given my actual trading frequency and position sizes?' That calculation produces a number; the spread label produces a marketing claim.

Impact on Scalping vs Swing Trading

For scalpers traders targeting small pip movements with high frequency the spread cost is disproportionately large relative to the profit target on each trade. A scalper targeting a 3-pip move on a pair with a 1.2 pip spread needs the trade to move 1.2 pips just to break even. That is 40 percent of the target consumed by execution cost before the market has moved at all.

On a raw spread account with a $7 commission per round turn (equivalent to 0.7 pips on a standard lot of EUR/USD), the break-even threshold falls to 0.7 pips a 42 percent reduction in the cost required to reach profitability on each trade. Across a high-frequency trading day, this difference compounds into a material performance differential.

For swing traders holding positions for multiple days or weeks, the spread cost is incurred once on entry and once on exit a single round-turn cost spread across the holding period. The daily opportunity cost of the spread is lower, and the difference between a 0.8 pip and 1.2 pip spread may be less consequential than the quality of the entry itself or the management of the trade over its duration.

This interaction between cost structure and trading style is why the same broker account can be materially better value for one trader and neutral or worse value for another the account type needs to be matched to the trading approach, not selected on the basis of advertised spread labels alone.

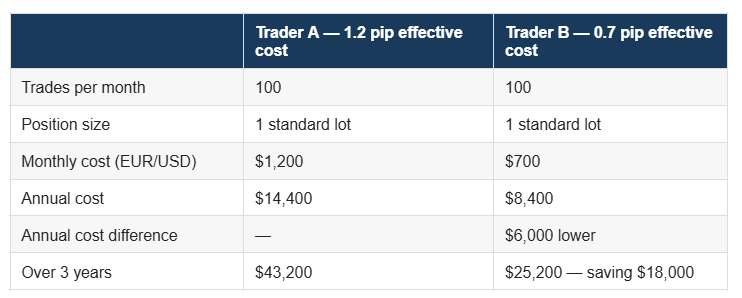

The Long-Term Compounding Effect: A Cost Modelling Example

To illustrate the compounding effect concretely, consider two traders executing identical strategies with the same win rate, average win, and average loss — differing only in their effective cost per trade.

The strategy is identical. The market conditions are identical. The only variable is execution cost and over three years, a 0.5 pip difference in effective spread produces an $18,000 divergence in cumulative cost. For a trader with a $50,000 account, that represents 36 percent of their capital consumed by cost differential alone.

Hidden Mark-Ups vs Transparent Commission

The cost analysis above assumes that the stated spread is the actual cost that a '0.8 pip spread' account delivers 0.8 pips of effective cost. In practice, that assumption requires scrutiny.

Hidden mark-ups can appear through several mechanisms: slippage on execution that consistently moves against the trader; spread widening during periods of high volatility that is not reflected in the quoted 'minimum' spread; re-quoting that delays execution until price has moved; and swap rates on overnight positions that embed additional cost beyond the stated commission or spread.

Transparent commission-based pricing, where the broker's compensation is a separate, fixed per-lot charge disclosed independently of the spread, makes these hidden costs easier to identify because the baseline cost is clear. When execution deviates materially from the stated commission plus raw spread, the deviation is visible and comparable.

The psychological appeal of a single cost number the spread is that it feels simple. The risk is that simplicity can conceal complexity in how that number is actually realised in execution.

How QuoMarkets Structures Its Raw Spread Accounts

QuoMarkets's raw spread account tier is built on direct liquidity provider pricing the wholesale interbank rate passed through to the account without additional markup layered into the spread. Broker compensation is taken through a disclosed commission per standard lot, applied as a separate line item rather than embedded in the quoted price.

This structure makes the cost calculation straightforward: the commission rate is stated, the raw spread reflects liquidity provider pricing, and the total cost per trade is the sum of those two components. For traders building cost models of the type described above, the inputs are explicit rather than estimated.

QuoMarkets provides the raw spread account alongside its standard account tier, allowing traders to select the cost structure appropriate to their trading frequency rather than applying a single model across all participants regardless of how they trade.

Conclusion

Small spread differences are not small in their cumulative effect. Applied across high trading volumes over meaningful time horizons, they compound into material performance differentials that are entirely within a trader's control to minimise through the choice of account structure, the alignment of that structure with their trading frequency, and the scrutiny applied to whether stated costs reflect actual execution quality.

The discipline of applying the same analytical rigour to cost modelling that traders apply to strategy development is one of the less glamorous but more reliably productive improvements available to active retail participants. The market provides no guaranteed edges; execution cost is one of the few variables that can be reduced through informed choice rather than predictive skill.